What types of clients would be bad fits for Guidance Point Advisors?

This is a question that we receive from time to time from our prospects. It’s a question our team debates about whether to answer on a blog. “We certainly don’t want to scare away potential clients, right?” But ultimately, we feel that we want our clients to be a really great match for our team and how we work.

If clients are asking us to do things that are not our strengths, or we’re simply not interested in performing, it leads to us not providing the best customer service we possibly can. It’s tough to fake it when you’re not passionate about the client or their needs. The point of this blog is to write as openly and honestly as we possibly can. If we don’t answer the hard questions, we’re simply not being honest with YOU. And YOU are the reason why we write.

The In And Out Client

What is an “In and Out Client”? This is a client that really wants the financial advisor to use their prophetic abilities to know what day is the best to fully invest their money and “get in” the market and then “get out” before something bad happens. The very difficult part of this type of activity is it means the investor needs to be right twice. One has to “get in” the market at the right time and “get out” at the right time.

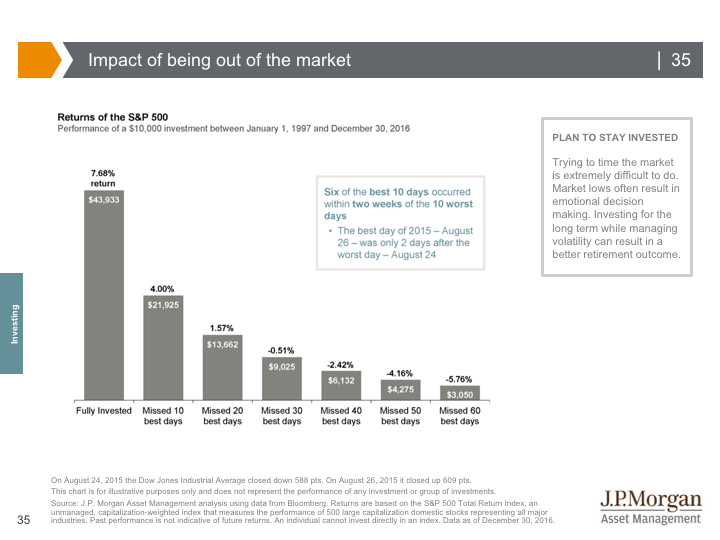

We see peers that do perform this activity, but we believe that any success is from luck and not from skill. Additionally, there may be lots of cost in order to perform this strategy. Are there commissions every time one buys or sells a stock, fund, etc.? If you have lots of investments in your account this activity can be very expensive. Also, if your account is subject to taxes you may be subjected to a large tax bill. See the chart below for a data point of the impact of being out of the market and how missing just 10 of the best days of the market over 20 years can be very costly.

The Penny-Penny-Penny Investor

Any viewers of the popular Big Bang Theory show on CBS will get this reference! In this case, we’re talking about penny stocks. Many investors are looking for the next big thing and are looking to scour penny stocks to find the next Apple or Google or Walmart. Unfortunately, many of the companies listed as penny stocks have various problems associated with them and success can be very difficult to find. When working as fiduciaries for our clients, we want to give them our best investing ideas. Unfortunately, penny stocks are very speculative (meaning high chance of failure) and just don’t fit our strategies for mapping out successful investment outcomes. Read more on Investopedia for some fallacies on penny stocks.

The “Look Ma, No Hands” Client

When working with our clients, we dedicate a significant amount of our time with each client educating them on the dynamics and levers of their investable assets and net worth. We want clients to understand what can cause successful outcomes, but also what activities can lead to unsuccessful outcomes. For example, if a client’s financial plan prescribes spending a range of $45,000 to $55,000 in retirement and upon retirement begins to spend $70,000 there will be a problem. If, and most likely when, the client runs out of money, this will lead to very difficult conversations because at this point the damage that is done is irreparable and the finger pointing / blame game starts. Clients that don’t engage with their advisor and simply say to them “just manage my money” is taking too passive of an approach and may be undertaking activities that lead them to suboptimal retirement or wealth outcomes. Look, its ultimately YOUR money and simply having a “hands off” approach may lead to danger down the road as you and your financial advisor make assumptions about your financial condition and long term satisfaction.

The Client that buys the plane ticket and demands to fly the plane, too

As we just described the client that takes too much of a hands-off approach, this type of client has too much of a hands on one for our liking. This type of client tends to second guess every decision and spends much of their time micro-managing their financial advisor.

This is the squeaky wheel syndrome for a financial advisor as they must spend a significant amount of time tending to the worries of one client and then spend less time for the remainder of their client base. In our view, its very unfair to our client base to accept this type of client as it takes away our time from supporting everyone.

Additionally, if the client truly doesn’t trust the decisions and processes of the advisor and firm they hired, then why are they with them? Why would the client pay the advisor an ongoing fee if they really are going to second guess the expertise? This is the type of client that really should be doing their own work and perhaps paying hourly an advisor to weigh in on decisions when needed.

Look, our team is happy to meet with our clients and set service expectations on how often we’d like to touch base and meet. This level of service is priced into our quoted fee to the client. When the client and financial advisor have different levels of service expectations, this is where client relationships can have issues. If we detect this happening with a client over time, that’s where we will have the conversation with the client and honestly let them know that servicing is not in line with the pricing and we would change the level of price to reflect the time spent. Honestly, we’d rather be pricing to the services that we ARE providing than charge a much higher fee for services we COULD provide. We believe this is one of the core differentiators of our fees.

Conclusion

There’s a saying in real estate that there’s “a house for every mouse”. And this is certainly true when picking a financial advisor. Making sure that your service expectations, investment philosophy, and values are aligned with who you choose to manage your money is very important. Also, for us at Guidance Point Advisors, we also want to make sure that our clients are fits so that every client past, present or future gets the best of us all the time. That’s what they deserve, and that’s what they should expect.

Are you searching for a financial advisor? Be prepared! Know what to look out or, and what questions to ask.

If you liked this blog, be sure to check out the following:

What Happens At A Financial Planning Meeting?

Choosing A Financial Advisor Part 1: Fiduciary or Broker?